Global share markets mostly fell over the last week as “higher for longer” interest rate signals from the Fed and some other central banks pushed bond yields higher. A 2.9% fall for the week took the key direction setting US share market below its August lows establishing a downtrend from July. Eurozone shares lost 2% and Japanese shares fell 3.4% but the Chinese share market rose 0.8%. Reflecting the weak global lead, the Australian share market fell by 2.9% for the week. Bond yields rose on the back of higher for longer interest rate expectations, with the US 10-year bond yield rising to its highest since 2007. Oil prices rose but metal and iron ore prices fell. The $A rose slightly, as did the $US.

The risk of a further correction in shares remains high with the main threats being: many central banks still leaning hawkish and warning of higher rates for longer; sticky inflation; rising bond yields pressuring share market valuations; the high risk of recession; the rebound in oil prices; China’s economy still at risk; the very high risk of a US Government shutdown from 1 October; continuing geopolitical tensions; and the weak seasonal period for shares into next month. However, our 12-month view on shares remains positive as inflation is likely to continue to trend down taking pressure off central banks and any recession is likely to be mild.

Central banks at or near the top – but many signalling higher for longer. A key reason why we are concerned about a further correction in shares is that central banks whilst likely at or near the top are still leaning hawkish, particularly in terms of staying restrictive for longer, which is maintaining upwards pressure on bond yields. More central banks left rates on hold over the last week (the Fed, BoE and central banks in Switzerland, Taiwan, the Philippines, Indonesia, South Africa and Japan) than hiked (central banks in Norway, Sweden and Turkey) but most retain a tightening bias with several signalling higher for longer rates. In particular:

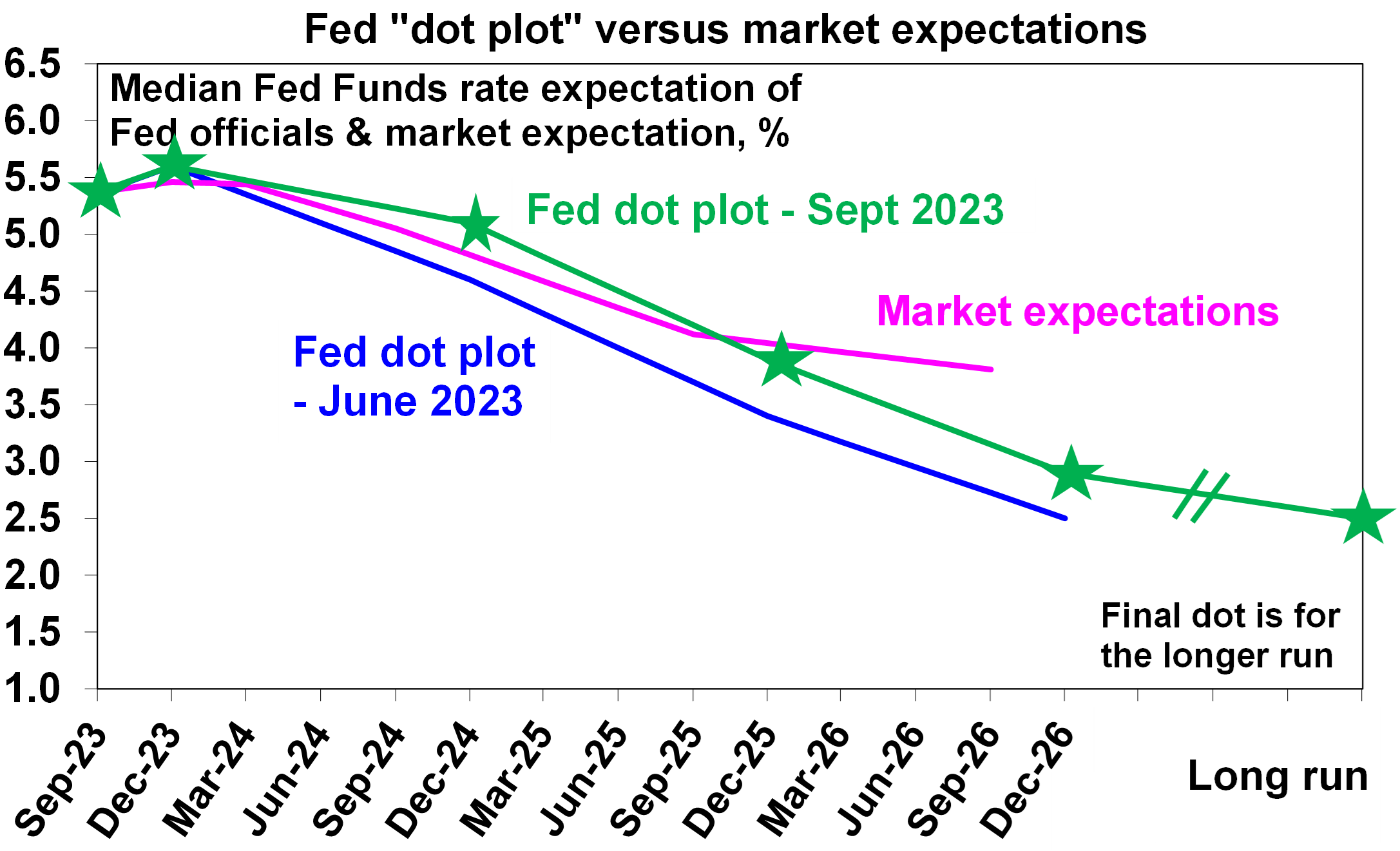

- The Fed left interest rates on hold but is still allowing for one more rate hike in its median “dot plot” of Fed officials interest rate expectations and raised its median “dot plot” expectations by 0.5% for each of the next two years on the back of upgraded growth and lower unemployment forecasts and despite still seeing inflation return to target by 2026. So, its expected pace of rate cuts over the next few years is substantially reduced. Our assessment is that the Fed’s growth forecasts are too optimistic and recession risk for next year remains high particularly as still rising bond yields will weigh even more on growth. But for now the “higher for longer” rates message is serving to push bond yields up even higher.

Source: Bloomberg, AMP

- The Bank of England left interest rates on hold at 5.25% in a dovish surprise, but the decision was close and it retained a tightening bias with Governor Bailey saying its “premature” to talk of rate cuts.

- The Bank of Japan left monetary policy on hold with comments by Governor Ueda suggesting rate hikes are still some way off.

- Canadian inflation rose more than expected in August – from 3.3%yoy to 4% with underlying measures also up – increasing expectations the BoC will hike again (from 5%).

- In Australia, the minutes from the last RBA meeting noted that while it left rates on hold it did consider hiking again and reminded that some further tightening may be required. Our view remains that the cash rate has peaked but the risks are skewed to another rate hike in the months ahead particularly given the risks of a near term uptick in inflation from higher fuel prices and the upside risks to wages growth. Given these risks we have decided to push out our expectation for the first rate cut from around March next year to around June.

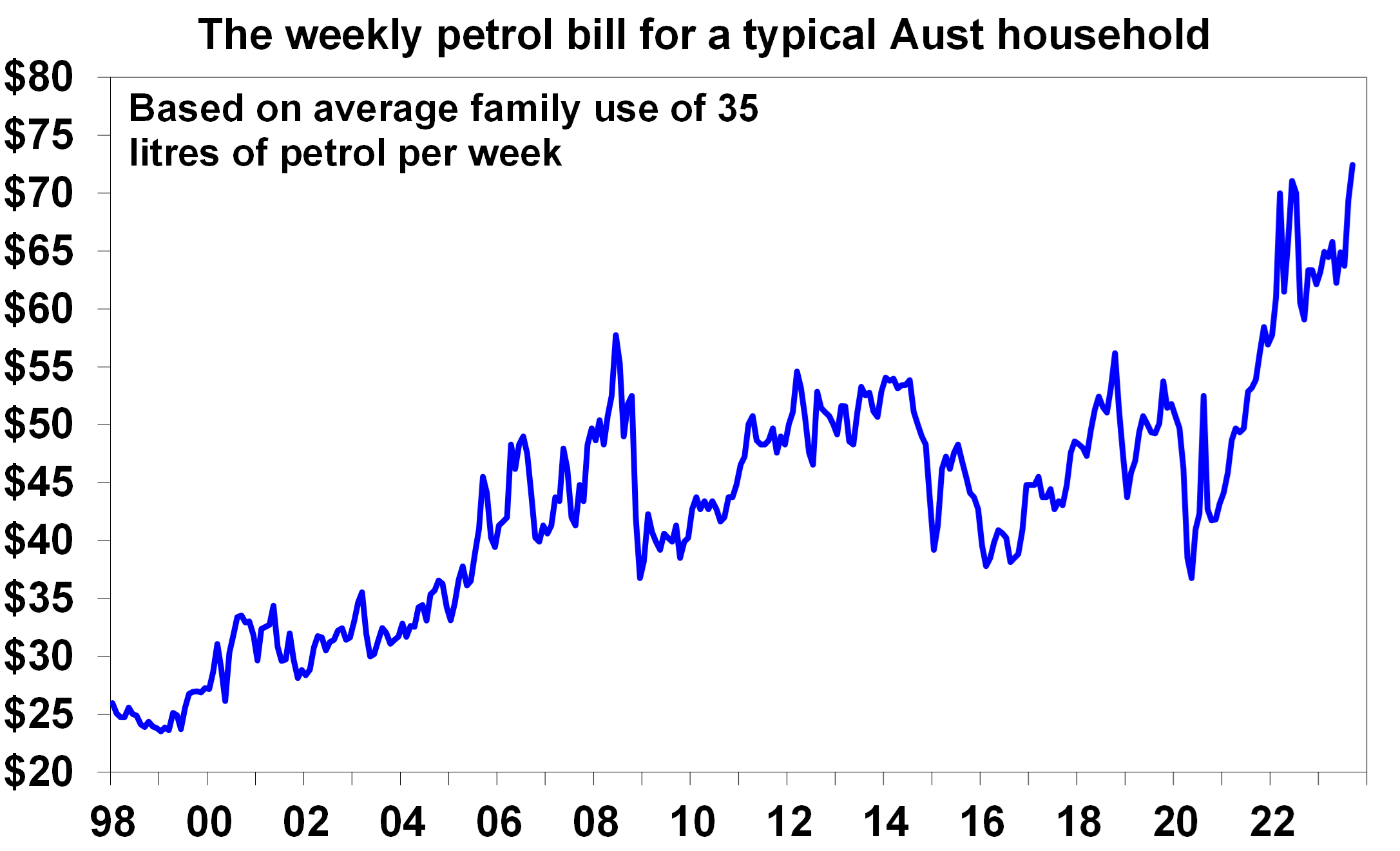

The downtrend in inflation has seen a bit of a reversal in some countries in August (notably in Asia, the US and Canada) thanks particularly to higher fuel prices. Consistent with this August inflation data in Australia to be released on Wednesday is also likely to show a tick up (to 5.3%yoy from 4.9%) with petrol prices up 9% in August.

Source: Bloomberg, ABS, AMP

The continuing surge in global oil prices to back above $US90 may be more of a threat to growth than inflation. On the one hand this is inflationary and will worry central banks. But its very different to 18 months ago when everything was going up in price and reopening (from Covid lockdowns) demand from consumers & businesses was strong. Now the reopening boost is well behind us, so this time around the surge in oil prices may act as more of a tax on spending and hence as a dampener on growth, which in turn could limit how far oil prices rise (although another production cut from Russia designed to hurt the West over its support for Ukraine is a high risk). On our estimates the average weekly household petrol bill in Australia has now increased by $10 since its recent low in May as petrol prices have pushed to record levels and this will mean a further reduction in household spending power. And so, our broad view remains that the trend in inflation will remain down.

Source: Bloomberg, AMP

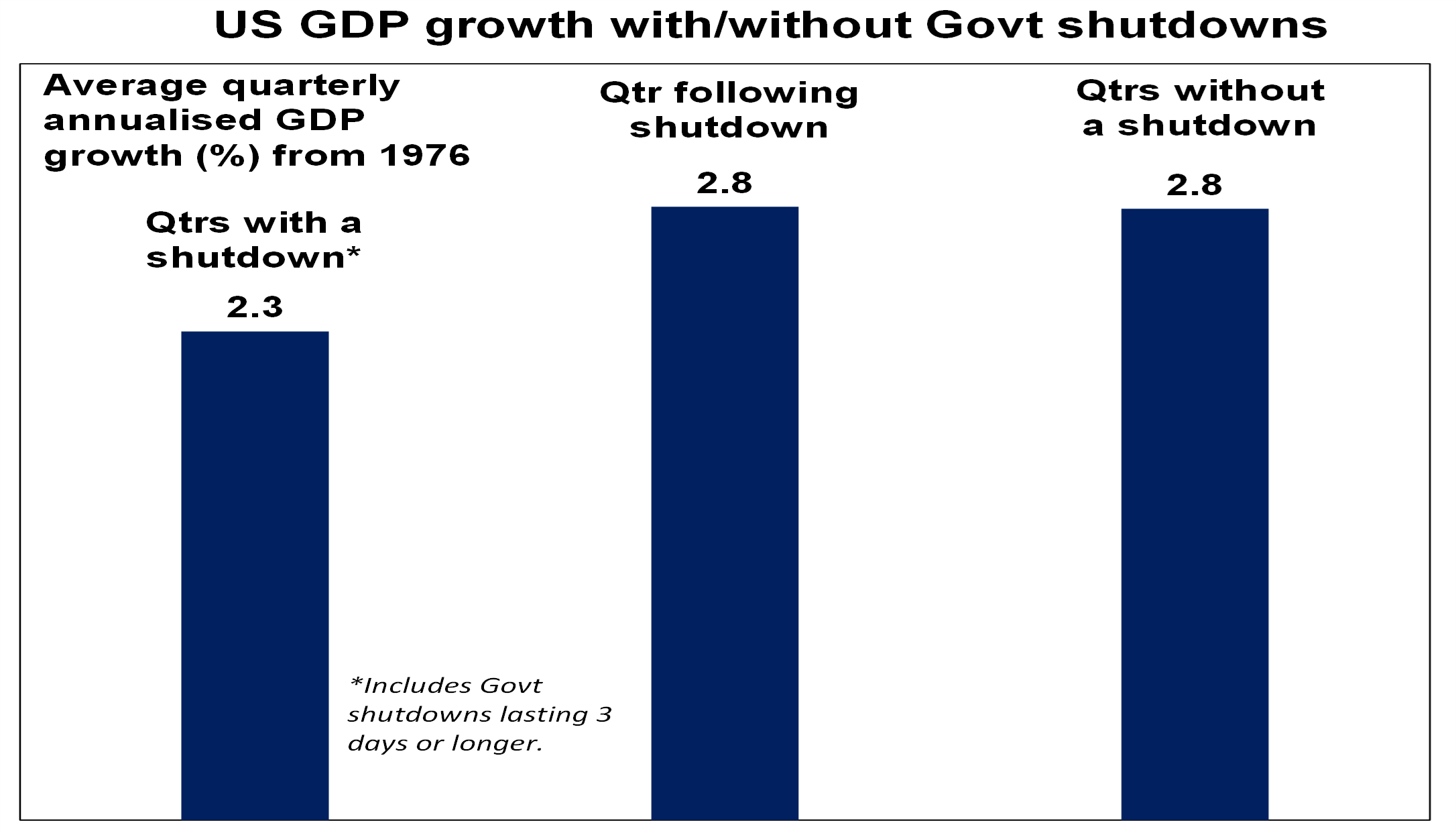

A US Federal Government shutdown is now a very high risk, but in the past their impact on economic activity has been minor. Put simply Congress needs to pass a new budget or a continuing funding resolution by 1 October to avoid a shutdown. House Speaker McCarthy is under high pressure from conservative Republican’s to hold firm in demanding reduced spending and the rising budget deficit and risk of another credit downgrade (which could occur due to a shutdown) is adding to the pressure. Since 1976 the US has had 21 government shutdowns with an average duration of around 8 days ranging from 1 day up to 35 days (which was in 2018-19). Usually, they are only a partial shutdown of Government and their economic impact tends to be minor with a catch up including in public servants pay after they end. Since 1976 quarters with shutdowns of 3 business days or longer averaged GDP growth of 2.3% annualised versus quarters with no shutdown having 2.8% annualised growth, which means an average difference of just 0.14% at a quarterly rate. When economic conditions are already uncertain like at present a shutdown now could add to share market volatility particularly if Moodys (the remaining top 3 ratings agency to still have US debt rated at AAA) downgrades US Government debt as a result.

Source: Bloomberg, AMP

More measures to boost Australian housing supply with a focus on affordable housing are what we need – but are they realistic? NSW announced a $3.1bn in housing and planning investment package to boost housing supply. But Victoria took the cake with a plan to build 80,000 homes a year over the next 10 years with the Victorian Government centralising planning powers to build five storey units, simpler or removed planning controls for single homes and a 7.5% levy on short stays. The focus on supply and particularly affordable and social housing is to be welcomed and what we need. Out concerns remain that:

- First, we lack the capacity to build all the homes being talked about – eg we are currently struggling to supply 180,000 new homes a year, the Federal and state plan aimed for 240,000 a year and if all states adopted something similar to Victoria it would imply 312,500 new homes a year. Even with lots of smaller cheaper units thrown into the mix it will be a challenge. That said I accept the need for stretch targets!

- Second, approval processes need to be sped up but overriding local councils and hence communities too much is likely to result in a backlash as people realise the increased congestion and loss of open space the extra homes will entail.

- Third, we need to focus on the demand side too and keep immigration levels (which are now running at a record) at levels more consistent with home building capacity (and temporarily below that so we can reduce the housing shortfall).

- Fourth, more effort also needs to be put into decentralisation away from big cities on a long-term basis.

- Finally, the increase in homes on short stay apps is a problem – but a 7.5% levy on them as Victoria is imposing means an up to 7.5% increase in short stay accommodation prices and less people travelling to regions and holidaying in Victoria.

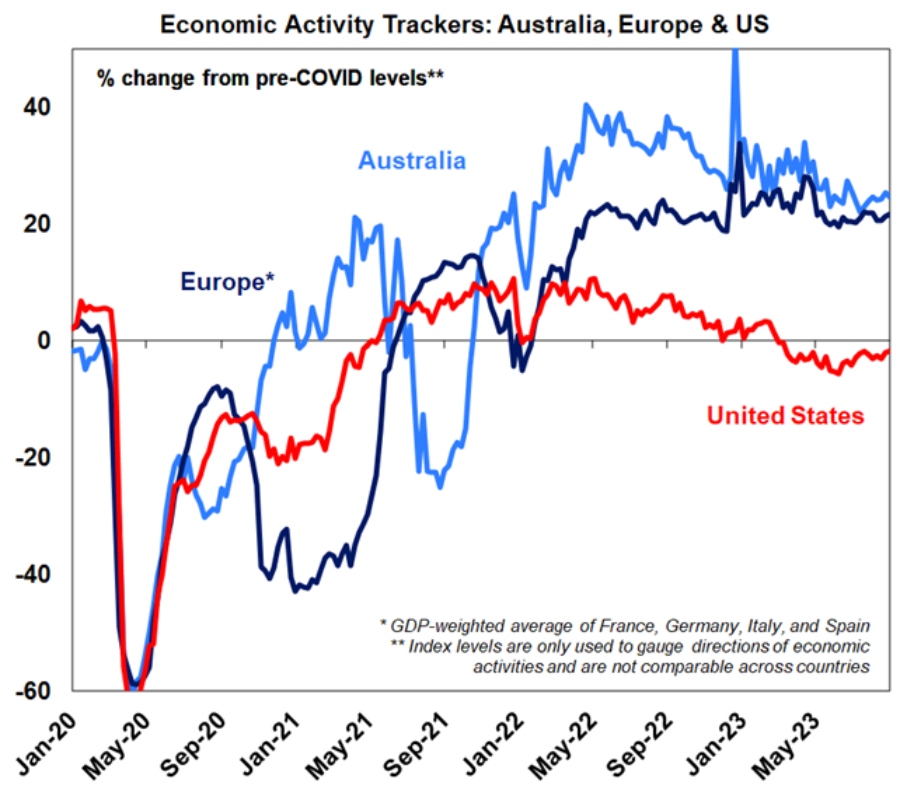

Economic activity trackers

Our Economic Activity Trackers are still not providing any decisive indication of recession (or a growth rebound).

Levels are not really comparable across countries. Based on weekly data for eg job ads, restaurant bookings, confidence, credit & debit card transactions and hotel bookings. Source: AMP

Major global economic events and implications

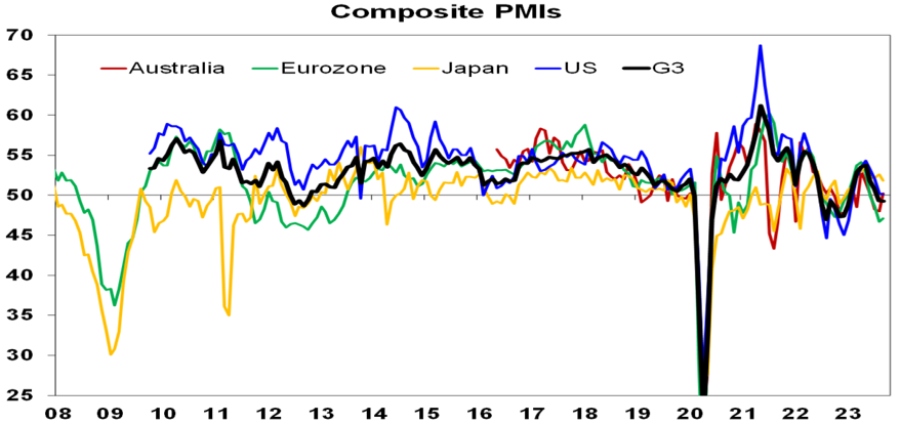

September business conditions PMIs (which are global surveys of businesses) were mixed across major countries, but little changed on average with manufacturing remaining negative and services soft. Overall conditions remain down from their highs earlier this year and are in a downtrend suggesting that growth is continuing to slow.

Source: Bloomberg, AMP

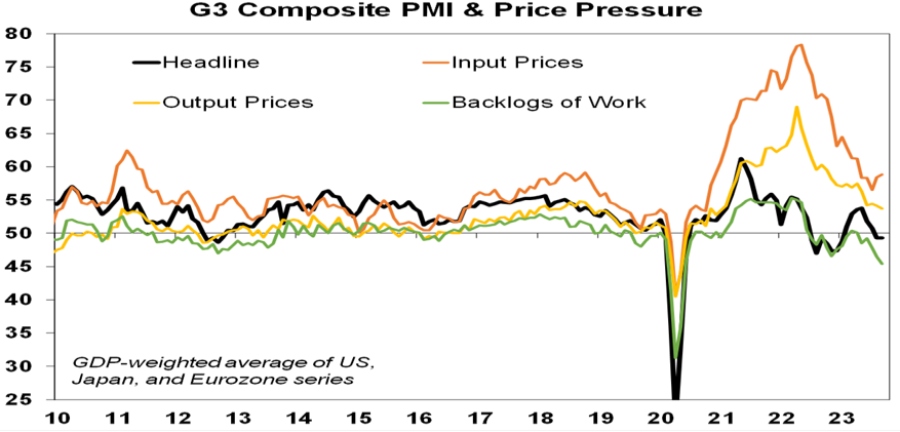

The PMIs also indicated that pricing pressures remain well down from their 2021-22 highs. Input prices generally edged up a bit again reflecting higher energy prices but output prices edged down, order backlogs remain down and delivery times remain much improved which is all consistent with an ongoing easing in inflationary pressures albeit there is still a way to go yet and energy costs remain a concern.

Source: Bloomberg, AMP

Apart from the PMIs, other US economic data was mixed. Jobless claims fell back to their lowest level since January adding to uncertainty about whether the jobs market is slowing (falling job openings suggest that it is). Against this though home building conditions fell in September, housing starts fell in August and existing home sales were weak as the rebound in mortgage rates impacts, manufacturing conditions weakened in the Philadelphia region and the US leading index fell again.

Japanese CPI inflation fell slightly to 3.2%yoy in August from 3.3% with core (ex food and energy) inflation unchanged at 2.7%yoy. Business conditions PMIs for September fell slightly with both manufacturing and services down but to a still ok 51.8.

New Zealand GDP growth surprised on the upside in the June quarter after two quarters of no growth. The strength was due to net exports and public spending but with soft consumer spending and falling dwelling investment. Its unlikely to tip the RBNZ into another rate hike.

Australian economic events and implications

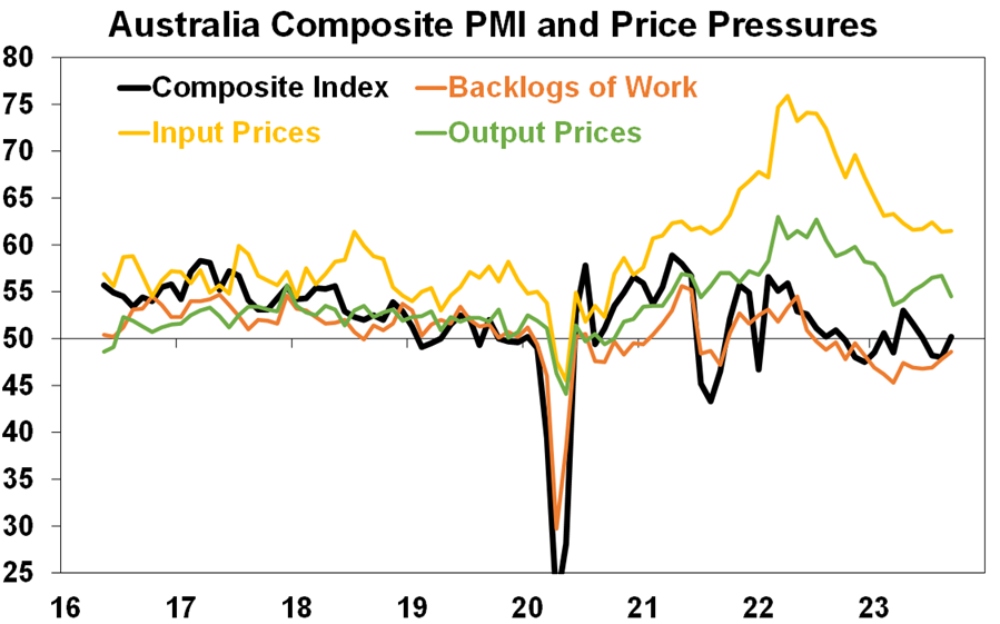

Australian business conditions PMIs for September rose again to the 50 growth/contraction level with a rise in services conditions. Cost pressures were flat, but output prices fell – both remain elevated but well down from their highs. Work backlogs are continuing to fall.

Source: Bloomberg, AMP

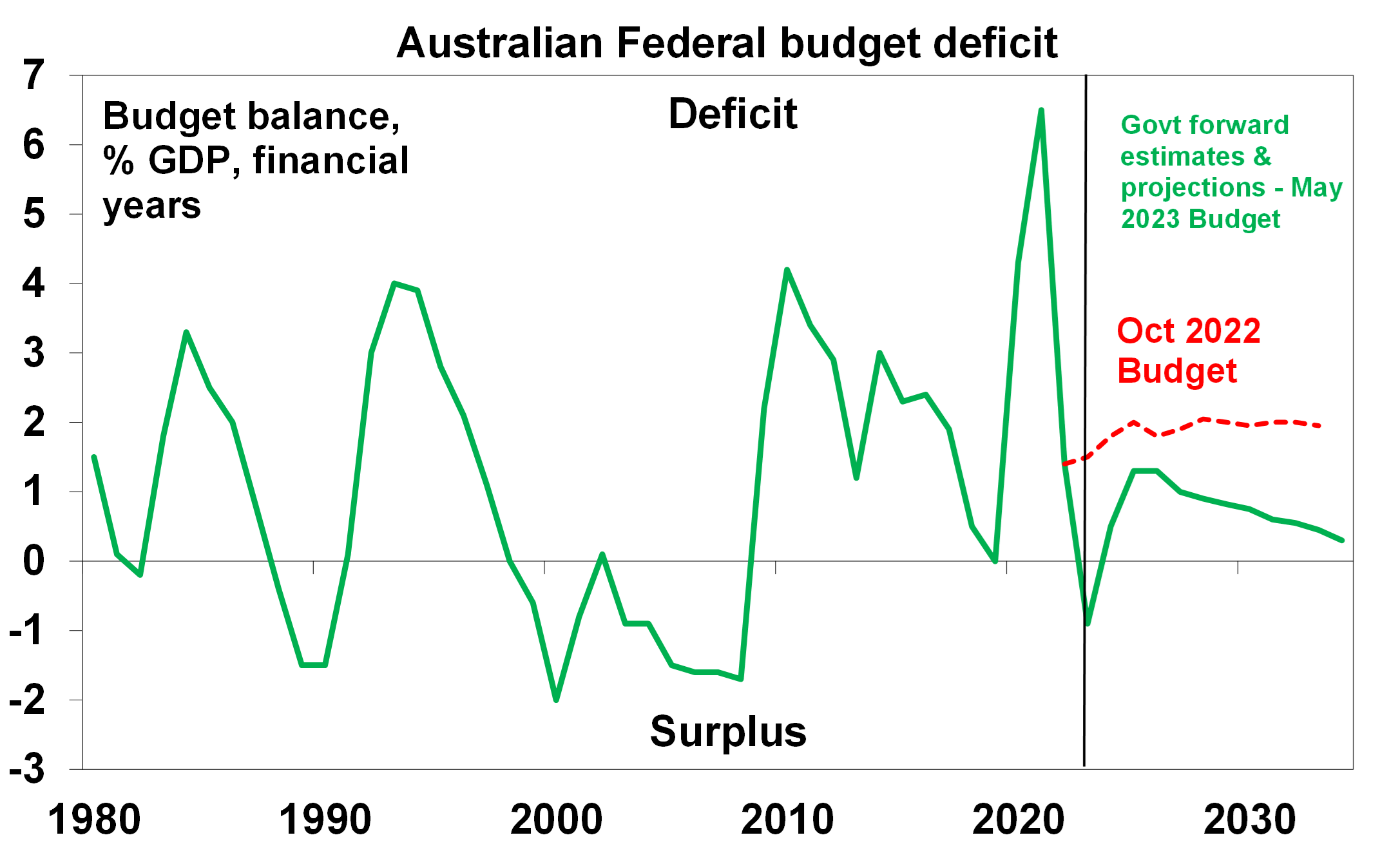

Australian budget confirmed to be back in surplus for 2022-23 – at $22.1bn. This is no surprise as May financial year to date data back in June showed a surplus of $19bn. The key drivers were higher taxes (from more people employed and higher than expected commodity prices) and less Government spending. This is a huge turnaround from a deficit of $99bn projected for 2022-23 just less than two years ago and is a far better situation than most other comparable countries that remain in deficit. That said given the strength in commodity prices the budget should be in surplus! Structural spending pressures from the NDIS, health, aged care, defence and interest payments will likely see a return to deficit but there is some chance of a small surplus this financial year rather than the $14bn deficit projected in May.

Source: Australian Treasury, AMP

What to watch over the next week?

In the US, expect a fall in consumer confidence but further gains in home prices (Tuesday), a fall in durable goods orders and flat capital goods orders (Wednesday) and a slowing in personal spending growth (Friday). Private final consumption deflator inflation for August (also Friday) is expected to rise to 3.5%yoy reflecting a rise in energy prices but core PCE inflation is expected to fall to 3.9%yoy from 4.2%.

Eurozone September CPI inflation (Friday) is expected to show a fall to 4.5%yoy from 5.2% with core inflation falling to 4.8%yoy from 5.3%. Economic confidence for September (Thursday) is likely to have weakened further.

Japanese industrial production for August is likely to show a rise with unemployment unchanged at 2.7% (both due Friday).

Chinese business conditions PMIs for September (due Friday and Saturday) are likely to be stable but relatively subdued.

In Australia, the monthly Consumer Price Inflation Indicator (Wednesday) is likely to show a rise to 5.3%yoy from 4.9% reflecting a 9% rise in petrol prices. August retail sales are likely rise 0.2% and job vacancies for the three months to August are expected to fall for fourth month a row (both Thursday) and housing credit growth (Friday) is expected to remain moderate.

Outlook for investment markets

The next 12 months are likely to see a further easing in inflation pressures and central banks moving to get off the brakes. This should make for reasonable share market returns, provided any recession is mild. But for the next few months shares are still at risk of a further correction given high recession and earnings risks, the risk of higher for longer rates from central banks, rising bond yields and poor seasonality out to October.

Bonds are likely to provide returns above running yields, as growth and inflation slow and central banks become dovish but given the recent rebound in yields this may be delayed a few months.

Unlisted commercial property and infrastructure are expected to see soft returns, reflecting the lagged impact of the rise in bond yields on valuations. Commercial property returns are likely to be negative as “work from home” continues to hit space demand as leases expire.

With an increasing supply shortfall, our base case remains that home prices have bottomed with more gains likely next year as the RBA starts to cut rates. However, uncertainty around this is high given the lagged impact of interest rate hikes and the likelihood of higher unemployment.

Cash and bank deposits are expected to provide returns of around 4-5%, reflecting the back up in interest rates.

The $A is at risk of more downside in the short term on the back of a less hawkish RBA and weak growth in China, but a rising trend is likely over the next 12 months, reflecting a downtrend in the overvalued $US and the Fed moving to cut rates.

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.